The Economy of Central Asia: A Fresh Perspective

10 November 2022

The report provides a renewed perspective on Central Asia as a large, dynamic and promising economic region and analyses its current structural changes and major growth areas

{kind=link}

{kind=link}

{kind=link}

EDB analysts studied the characteristics of the region’s countries, their prospects for cooperation and their development potential. The states have established themselves economically and have wide-ranging growth potential. Central Asia’s aggregate GDP totals $347 billion. Over the last two decades, the GDP of Central Asia grew more than sevenfold. The share of Central Asia in global GDP (PPP) has increased by a factor of 1.8 since 2000. Its population of 77 million has increased by a factor of 1.4 since 2000. The region’s growing population provides a capacious sales market, and generates an expanding pool of labour resources. Demographics definitely favour economic growth in Central Asia. The current age distribution points to a future growth of labour resources.

The average annual economic growth rate for Central Asian countries has been 6.2% over the past 20 years compared to developing countries’ growth rate of 5.3% and the world average of 2.6% per year. Growth of export revenues, remittances by migrant workers, and foreign direct investment contributed to the rise of incomes and reduction of poverty. In most countries of the region, GDP per capita at PPP increased threefold.

In 2021, the region’s foreign trade in goods totalled $165.5 billion, a sixfold increase over the last 20 years. Mutual trade between the countries is growing even faster than their total foreign trade.

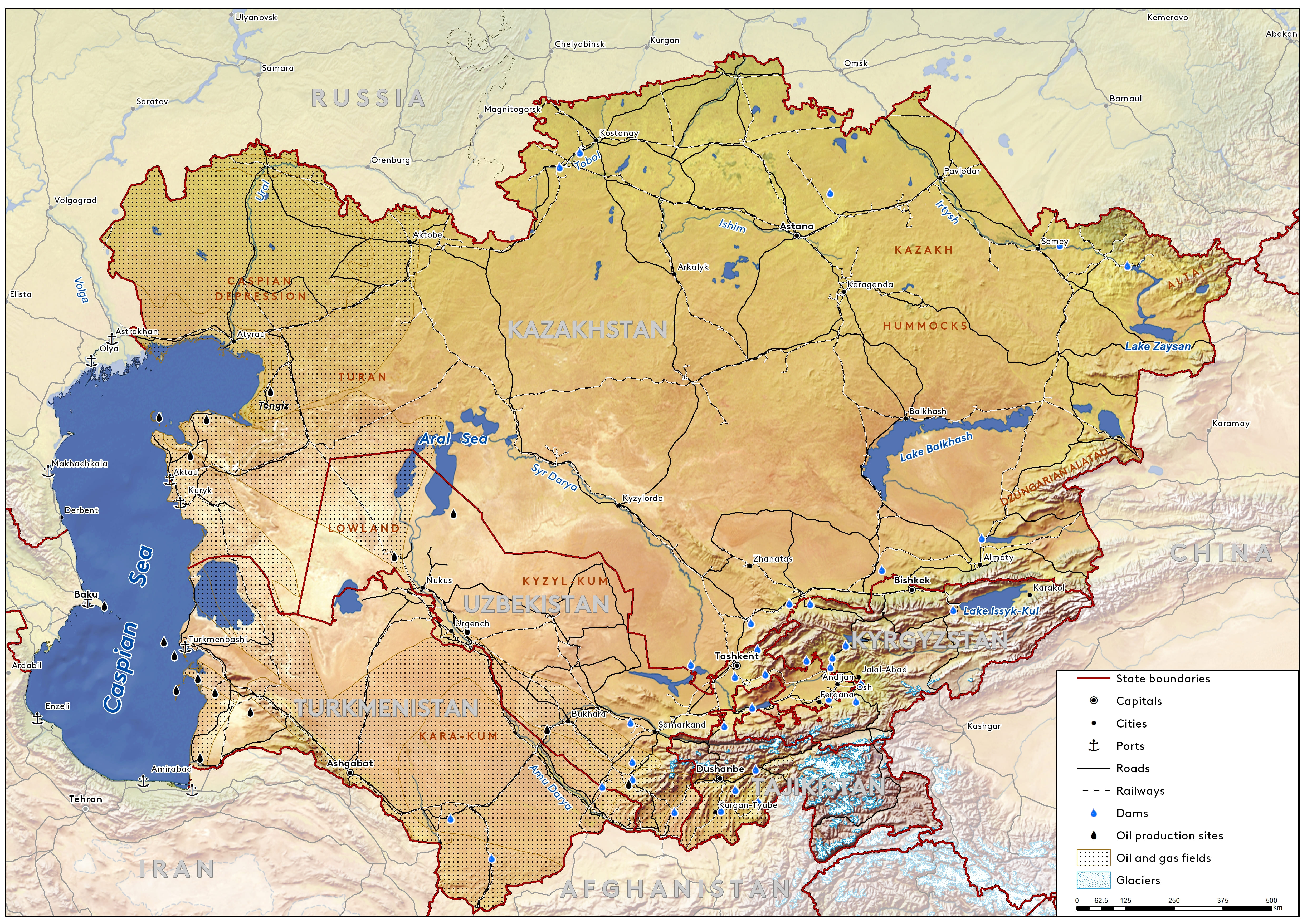

Inward FDI stock in Central Asia totals $211 billion. Over the past 20 years, this figure has increased more than seventeen-fold. While FDI in the region is growing, its structure, both country- and sector-specific, reflects certain challenges. The lack of openness of some of the countries, their remoteness from major economic centres and the fact that countries have no access to the world ocean continue to affect international investors’ perception of the region. The ratio of FDI relative to GDP, excluding investment in the commodity sectors, is below the global average, indicating that the region is underinvested.

The Region’s Achievements and Structural Changes

Source: EDB analysis based on national statistical agencies, central (national) banks, IMF, ADB, WB, Trade Map, CEIC.

Sustainable development in Central Asia requires a balanced approach to attracting external funding – through strengthening and promoting good relations between the region’s countries and implementing the regional programmes of international organisations and development banks. It will also require FDI in non-commodity sectors and for the countries to harness the potential of domestic savings.

The share of mutual trade between Central Asian countries in their total trade turnover is consistently increasing, having reached 9.9% by the end of 2021. Uzbekistan provided a powerful impetus to development and expansion of intra-regional trade after 2017.

Despite certain progress, there are several systemic problems that hinder the socio-economic development of Central Asian countries. Commodity exports and migrant workers’ remittances continue to play a major role in the region’s economies. Other significant issues include the quality of the institutional environment, bottlenecks in regional transport networks, social issues, macroeconomic risks and insufficient harmonisation in regional trade and economic relations.

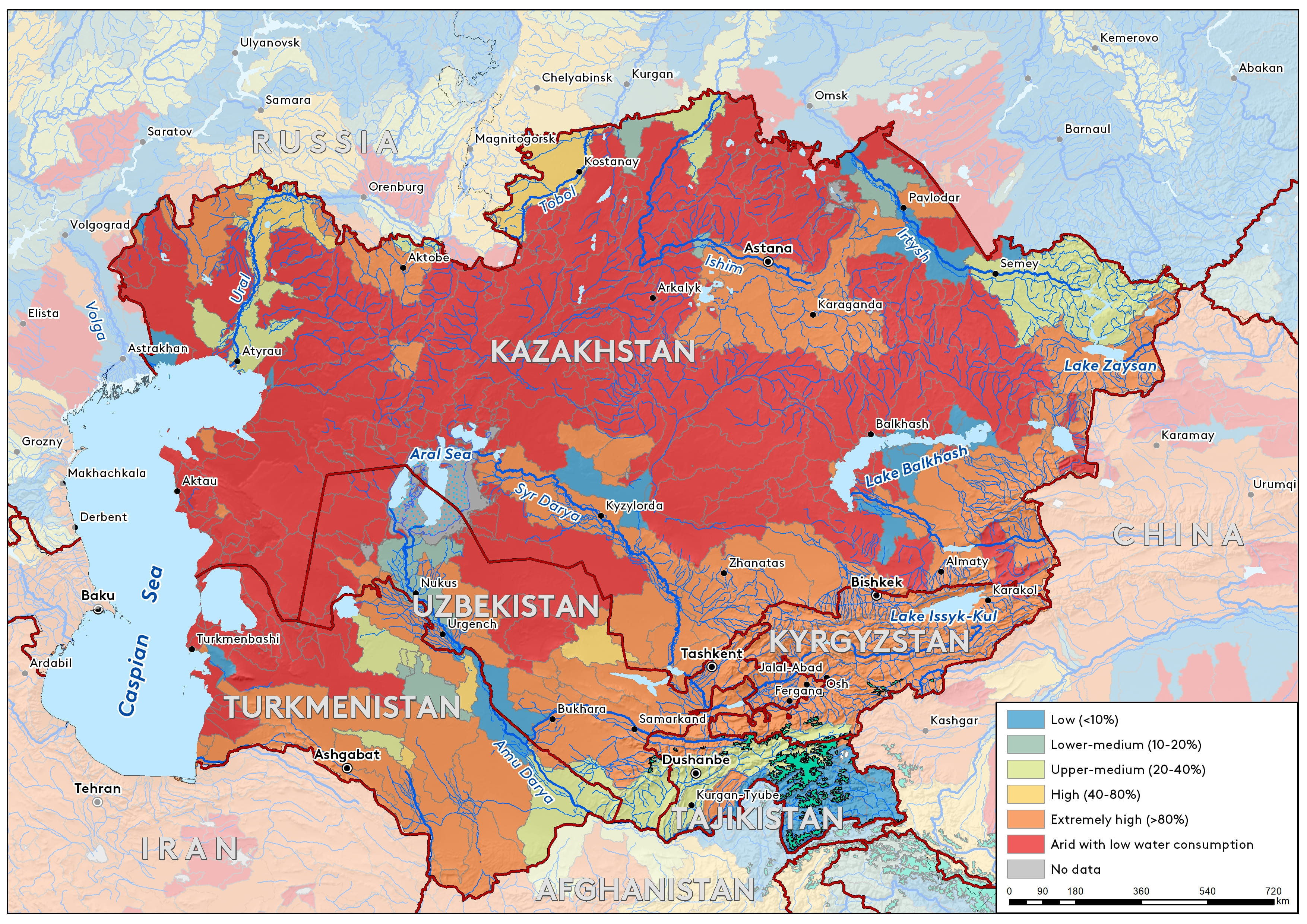

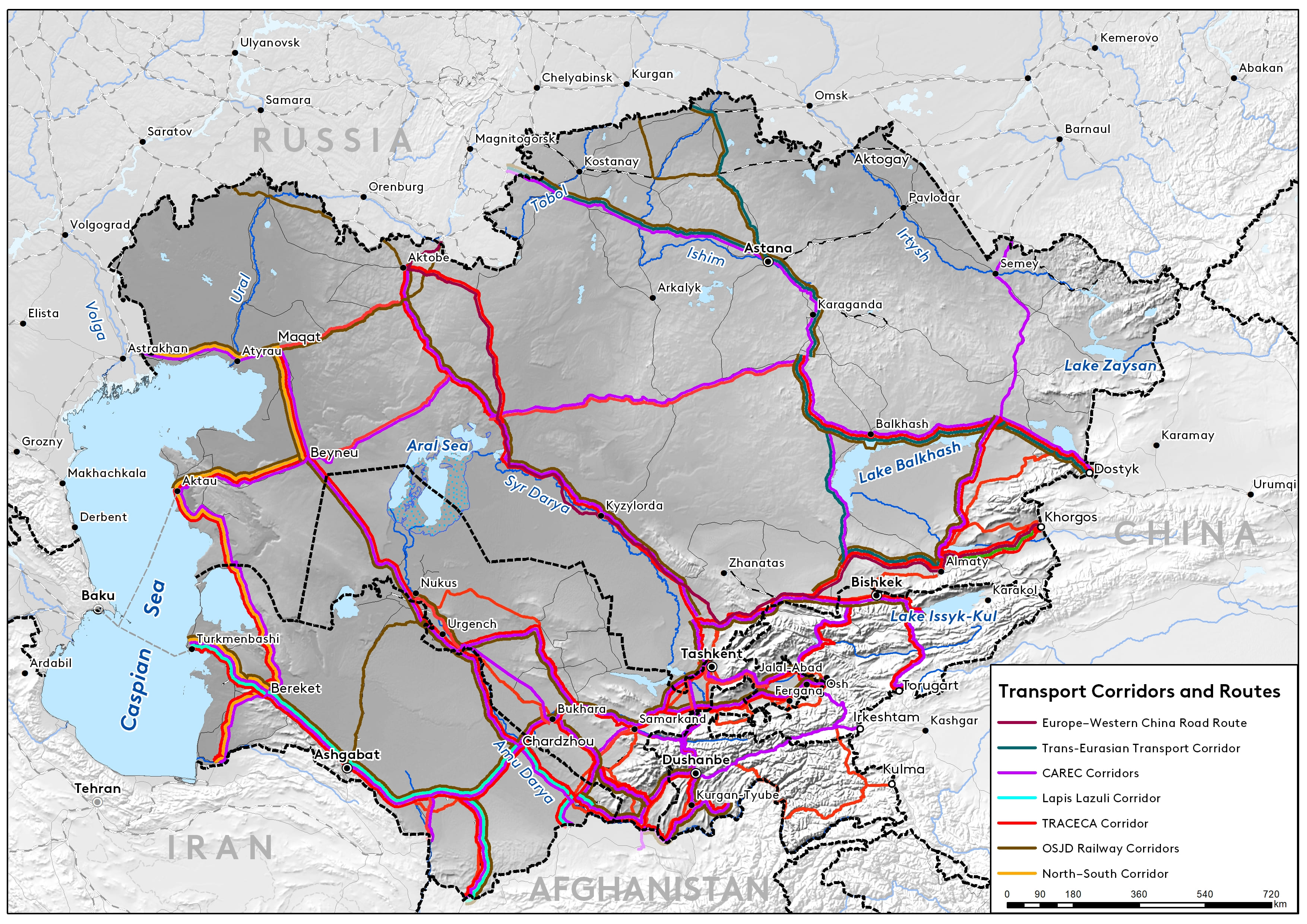

The region’s countries need to overcome four key structural challenges: lack of access to the sea, resource dependence and the low level of development of the financial sector, lack of coordination in management of the water and energy complex, and climate change. EDB researchers believe that, through concerted effort, Central Asian countries will overcome structural development problems. Increasing pressure on the energy system during a period of strong economic growth and the fact that the countries share river basins leave little option other than to cooperate in water and energy. Equally important are coordinated efforts to develop transport infrastructure and combat climate risk. Eliminating infrastructure bottlenecks will help to promote economic productivity, trade and economic partnerships with neighbouring countries, and encourage diversification of production and exports.

Structural Challenges and Mitigation Tools

Source: EDB

All copyrights and other intellectual property rights on this website page or in its content, including, but not limited to, figures and maps, are owned by the EDB. You may view, copy, or print the сontent for your own use only provided that all copies and prints of the сontent bear EDB copyrights or other mentions of the EDB intellectual property rights.